We’ve outlined the Discovery Bank credit application process to help you become familiar with the process and assist your clients with any queries they may have when joining Discovery Bank.

Applying for credit on the Discovery Bank app is a quick and seamless process. However, sometimes clients get stuck along the journey and may not know what to do next. That is why we have compiled an outline of the different phases in the credit application process, with information on what the client can expect to see and the documentation clients need to have ready to proceed, so that you can help them along the journey.

There are five distinct phases in the credit application process:

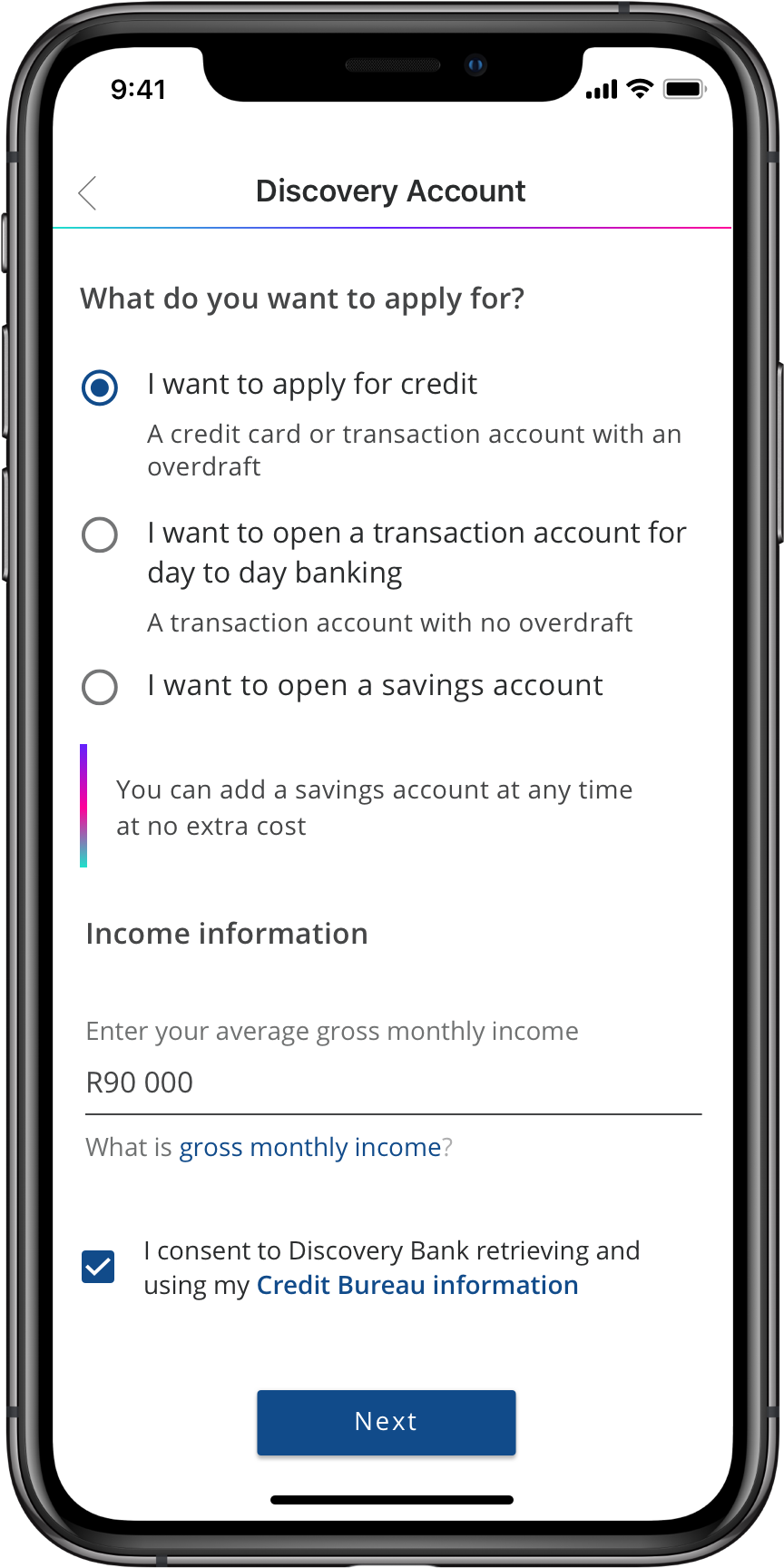

Phase 1: Application

During this phase:

- Your client provides Discovery Bank with their income information so that a relevant collection of products can be recommended

- Discovery Bank will ask your client for consent to use bureau data as the basis for the credit application

- Discovery Bank needs this consent to assess your client’s full financial portfolio and provide a suitable offer

- Without this bureau consent, your client can only apply for a savings account through Discovery Bank.

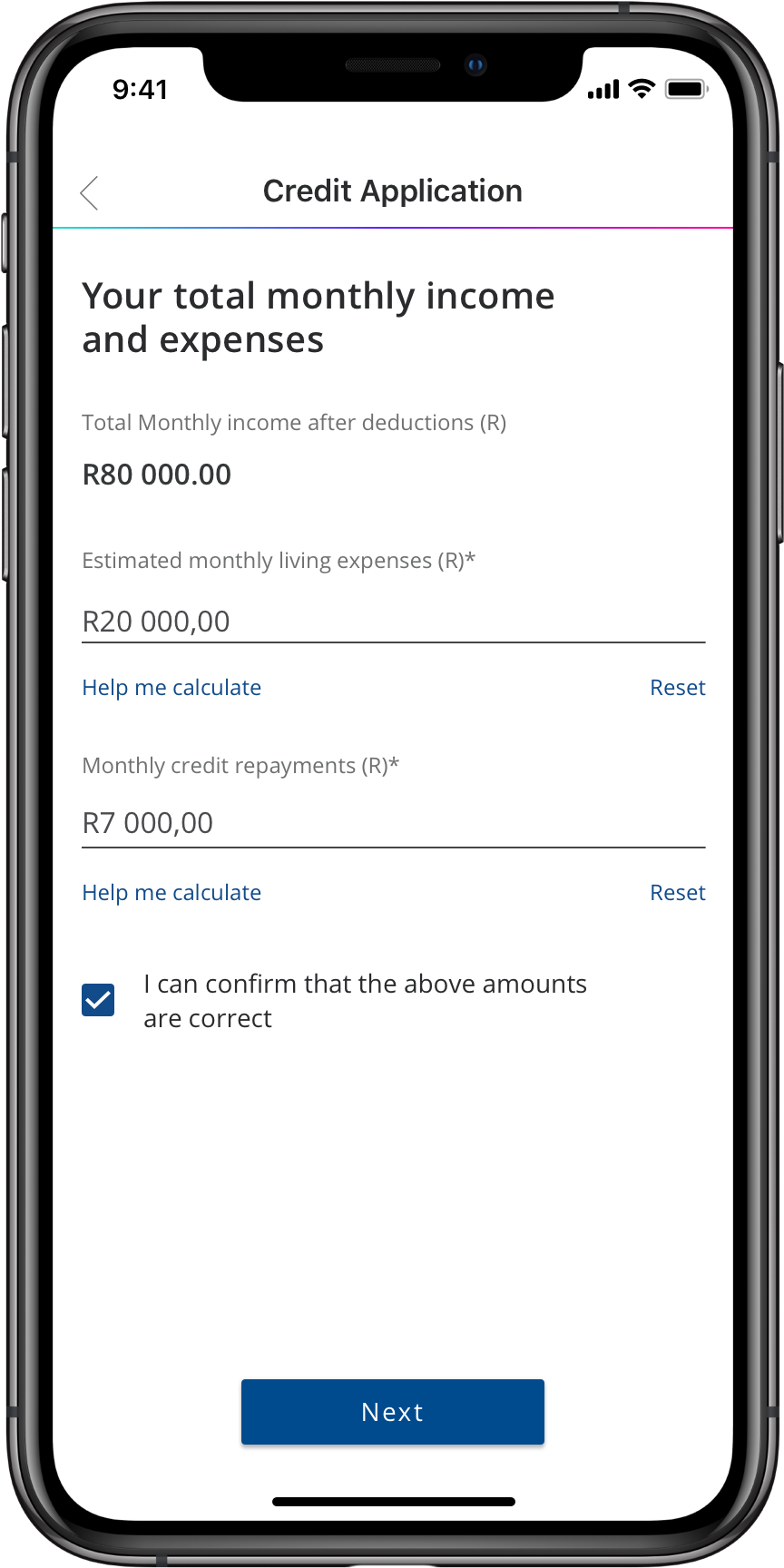

Phase 2: Credit assessment and offer

During this phase:

- Your client inputs important information to calculate their disposable income, for example: their monthly income, deductions and living expenses

- This information is reviewed and the application is assessed based on your client’s willingness and ability to pay

- Willingness to pay is measured by looking at a client’s risk profile and using credit bureau information to understand how they have conducted themselves in the past on other credit agreements. Based on this information we calculate the client’s credit score to determine if the client will successfully manage and repay the loan instalments. These checks also include eligibility rules that look at high risk indicators, rules to identify clients with very little or no credit history on the Bureau as well as rules to identify potential fraud

- Ability to pay, or affordability, is assessed by calculating a client’s monthly disposable income and determining if the client can service the new credit that Discovery Bank is willing to offer the client. Simply put, this is calculated as:

Disposable income = net income - living expenses - credit commitments

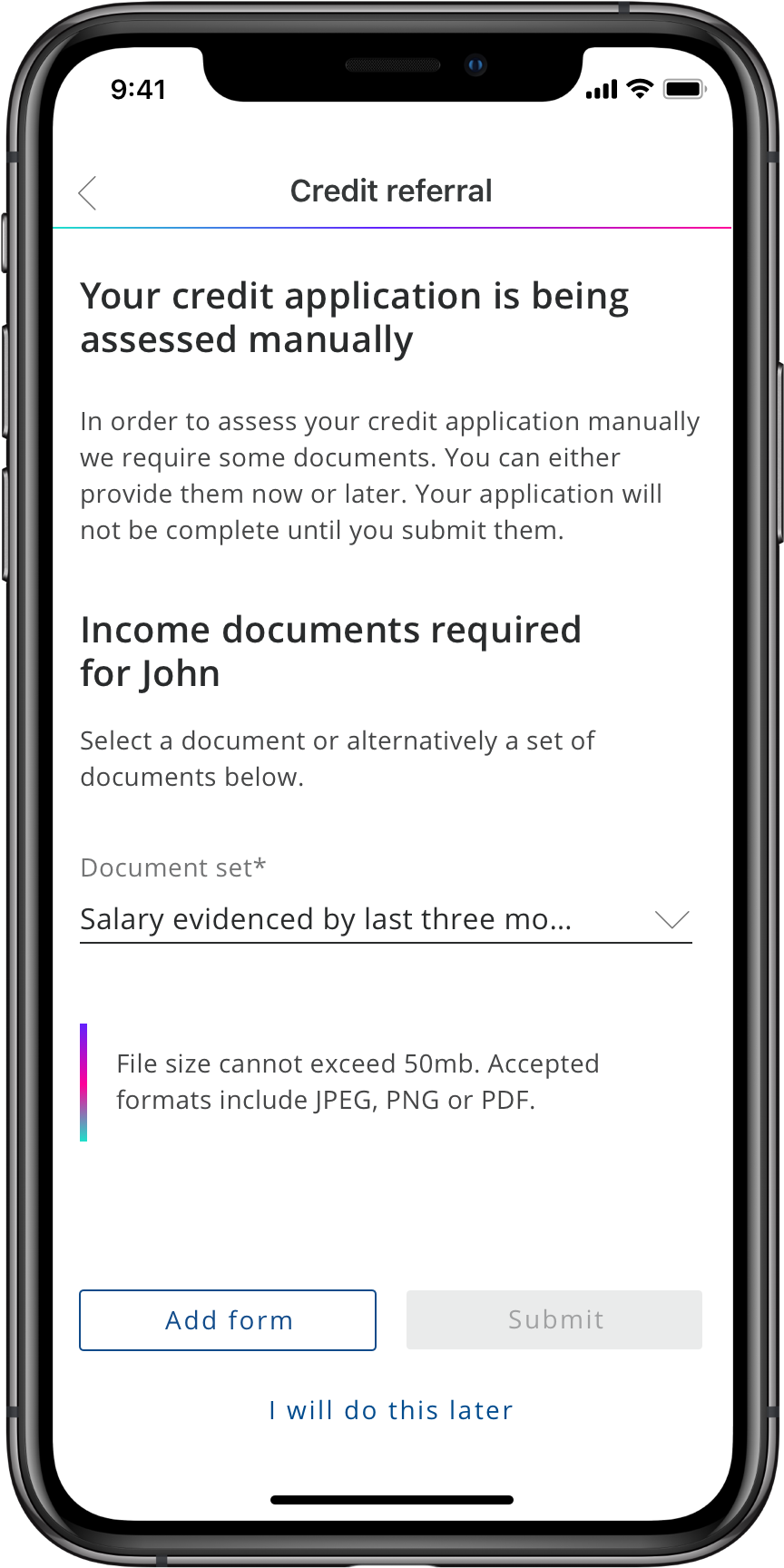

Phase 3: Verification

During this phase:

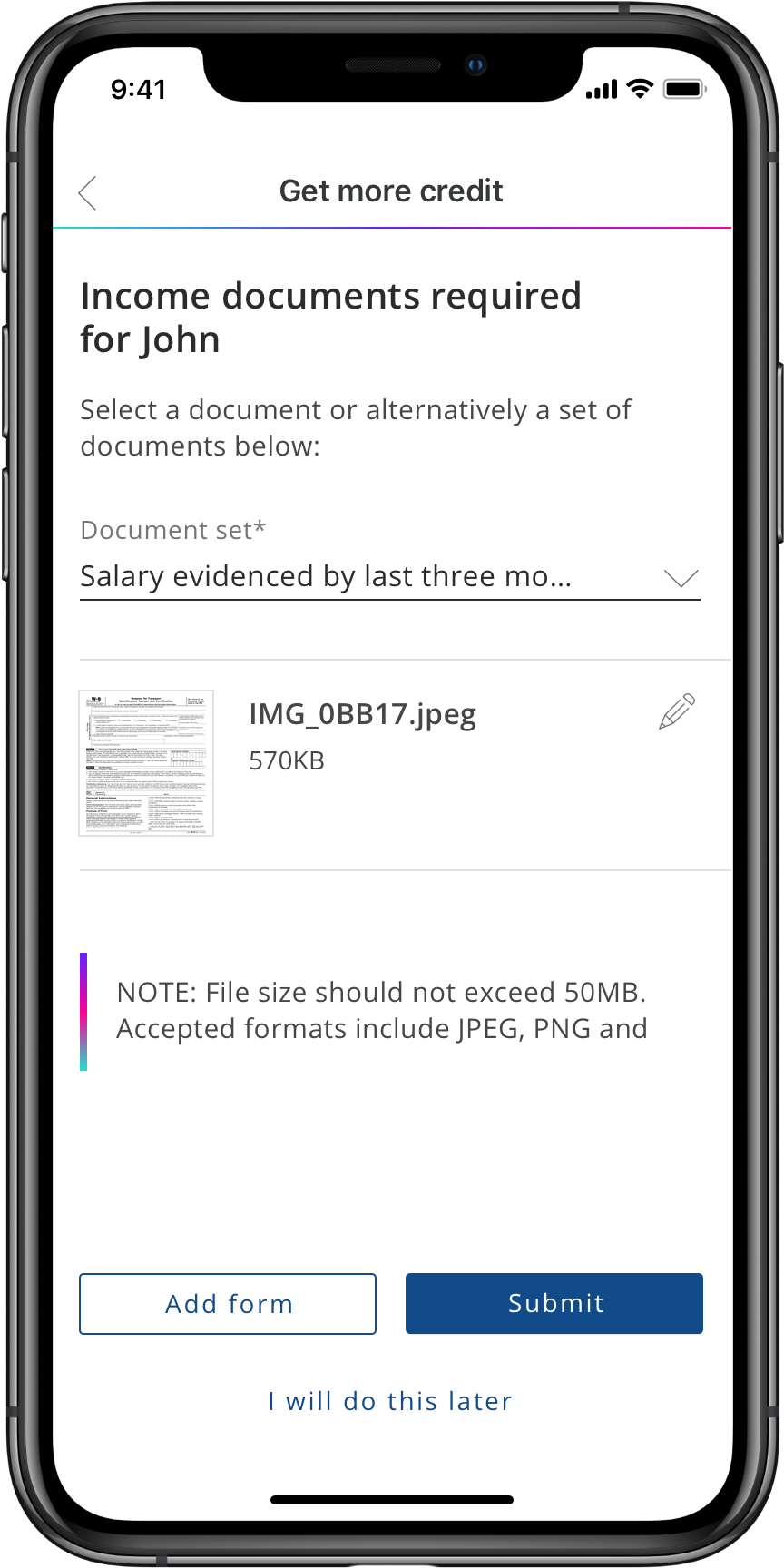

- Your client needs to provide the relevant documents to verify the information provided

- For most clients, they can submit one of the following as proof of income:

- Payslips for the most recent three months

- Bank statements for the most recent three months

- ITA34

- IRP5

- Documents are submitted by uploading it to the Discovery Bank app

- Clients can also submit documentation on the online.discovery.bank website

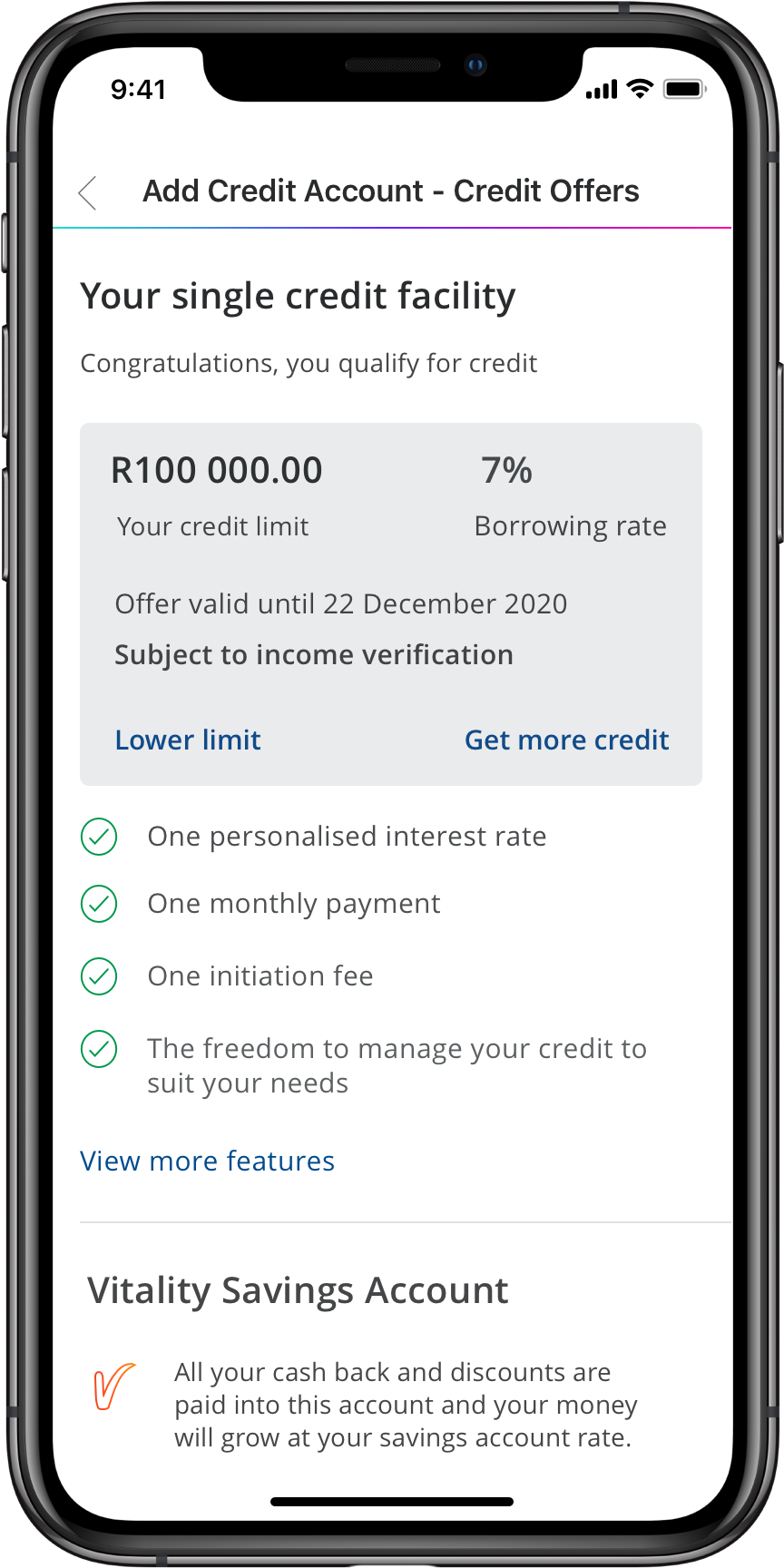

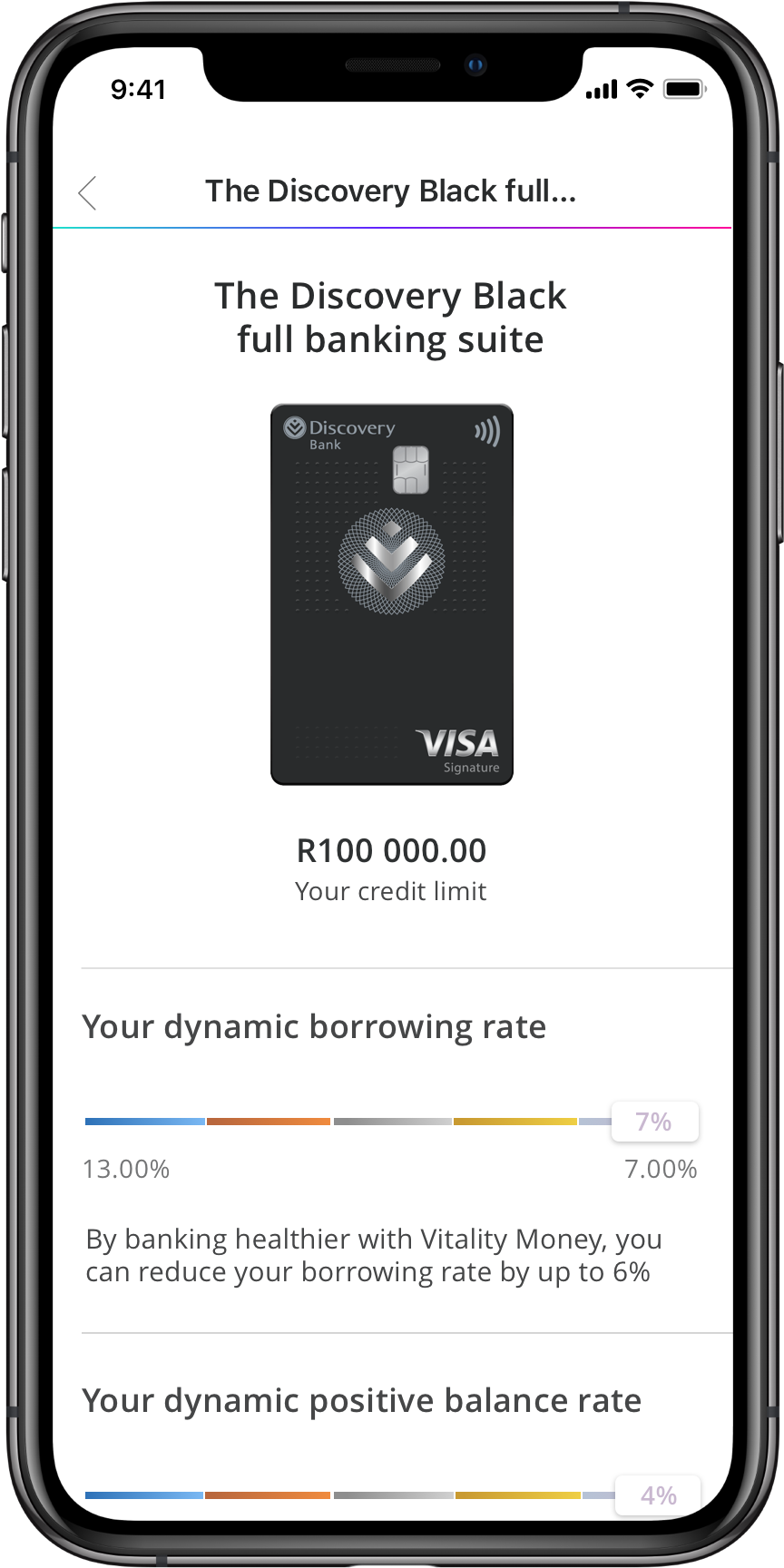

Phase 4: Credit contract

During this phase:

- Discovery Bank will offer your client a specific credit card and personalised rate based on the information provided

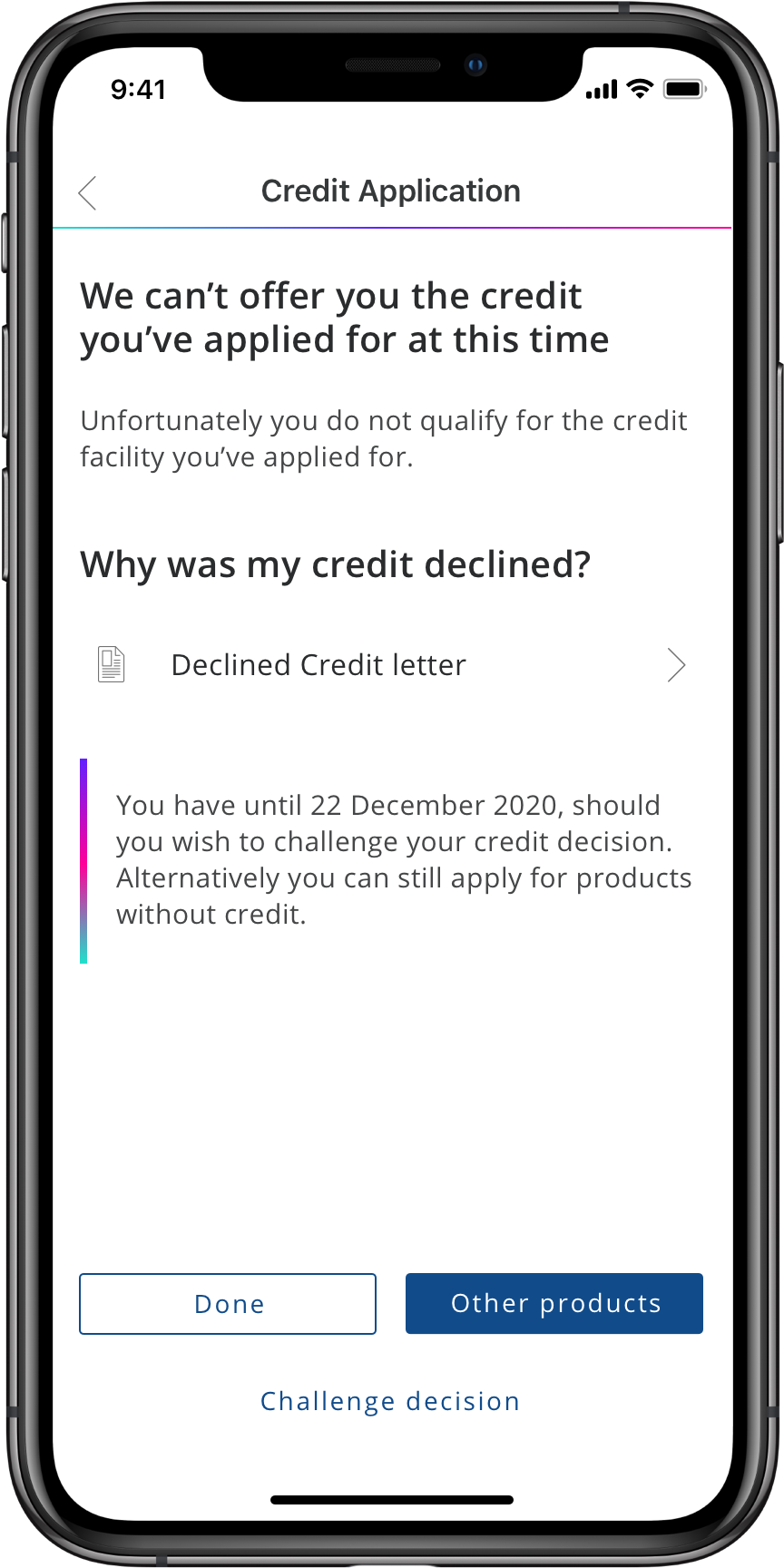

- During this phase the client can dispute the decision and ask for a higher limit or different offer by selecting Get more credit

- If your client is declined for credit, Discovery Bank will provide the client with a Declined Credit Letter which will outline the decision, the reasons why the decision was made, and actions your client can take to resolve or challenge the outcome.

Phase 5: Client origination

During this phase:

- Discovery Bank opens the agreed upon account and the credit facility is created

- The relevant cards are created and the card delivery process is initiated.

Common questions answered

Along with the basic documents, such as IDs, the client must have certain documents on hand.

For salaried individuals, we need one of the following:

- Payslips for the most recent three months

- Bank statements for the most recent three months

- ITA34

- IRP5

For commission earners, we need one of the following:

- Payslips for the most recent three months

- Bank statements for the most recent three months

- IRP5

Note: for most other sources of income, bank statements for the most recent three months are sufficient.

If clients don’t agree with a decline outcome, they can challenge the decision in the banking app. They will be asked to supply additional documents for income verification, as well as any other documents relating to the reason for the decline.

All documents uploaded in this challenge process will be routed to the Discovery Bank Credit Operations team directly. The client must initiate this and documents can be uploaded through the Discovery Bank app as shown below:

Tap Challenge decision

Select a reason

Upload supporting documents for further review

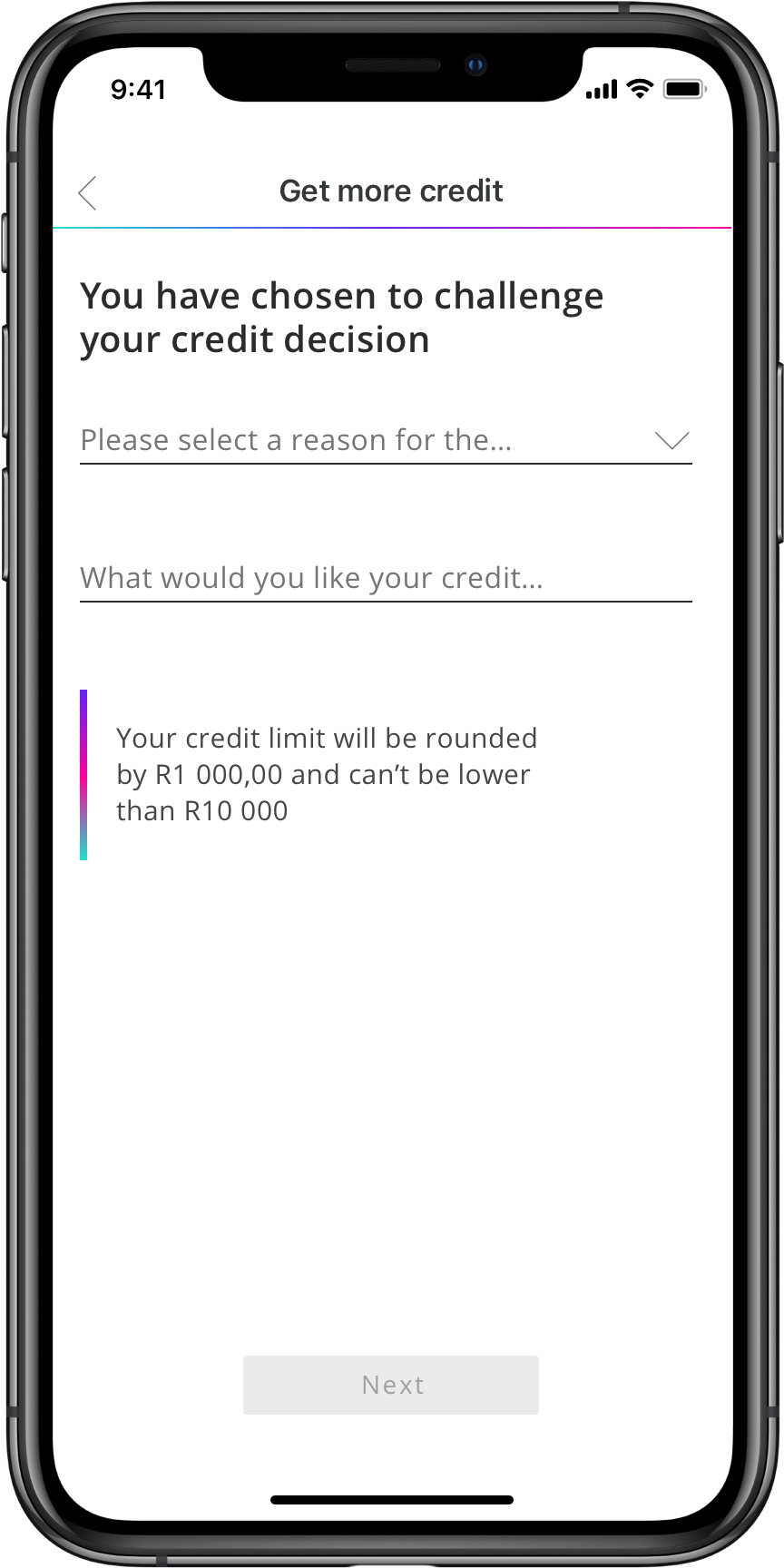

If a client wants a higher limit than the one offered by Discovery Bank, they can also challenge the offered amount on the banking app. Clients will be asked to supply additional documents for income verification as part of the dispute process.

All documents uploaded in this challenge process will be routed to the Discovery Bank Credit Operations team directly. The client must initiate this and documents can be uploaded through the Discovery Bank app as shown below:

Tap Get more credit in the credit offer screen

Select a reason

Upload supporting documents for further review

If your client needs more information or guidance, they can contact the Discovery Bank call centre on 0860 11 2265 (BANK).

However, while the call centre can assist with information and guidance, they cannot handle any disputes regarding declines or credit limits. If your client isn’t happy with the outcome they need to dispute and reapply on the banking app.

Need more information or support?

If you require any support or assistance, please contact your Partner Relationship Manager directly or submit your query to: distributionsupport@discovery.bank